Medicare premiums based on income in 2027 will be determined by your Modified Adjusted Gross Income (MAGI) from 2025. This means the financial decisions you make right now directly impact what you will pay for healthcare two years down the road.

If you are approaching retirement or are already enrolled in Medicare, the surcharge known as IRMAA (Income-Related Monthly Adjustment Amount) can come as a shock. It affects roughly 7-8% of beneficiaries—those with higher incomes—requiring them to pay more than the standard premium.

Quick Answer: 2027 Medicare Premium Projections

Based on estimated inflation and historical trends, here is what you can expect to pay in 2027 based on the income you earn in 2025.

Note: These are projections. CMS releases final numbersin November 2026. The standard base premium is projected to be $202.90/month.

Projected 2027 IRMAA Brackets (Part B & Part D)

Filing Status: Single, Head of Household, Qualifying Widow(er)

| 2025 MAGI Range | Part B Premium | Part D Surcharge | Total Extra Cost/Mo |

| ≤ $111,000 | $202.90 (Standard) | $0.00 | $0.00 |

| $111,001 – $139,000 | $284.10 | +$14.50 | +$95.70 |

| $139,001 – $174,000 | $405.80 | +$37.50 | +$240.40 |

| $174,001 – $208,000 | $527.50 | +$60.40 | +$385.00 |

| $208,001 – $500,000 | $649.20 | +$83.30 | +$529.60 |

| > $500,000 | $689.90 | +$91.00 | +$578.00 |

Filing Status: Married Filing Jointly

| 2025 MAGI Range | Part B Premium | Part D Surcharge | Total Extra Cost/Mo |

| ≤ $222,000 | $202.90 (Standard) | $0.00 | $0.00 |

| $222,001 – $278,000 | $284.10 | +$14.50 | +$95.70 (per person) |

| $278,001 – $348,000 | $405.80 | +$37.50 | +$240.40 (per person) |

| $348,001 – $416,000 | $527.50 | +$60.40 | +$385.00 (per person) |

| $416,001 – $750,000 | $649.20 | +$83.30 | +$529.60 (per person) |

| > $750,000 | $689.90 | +$91.00 | +$578.00 (per person) |

https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

What is IRMAA and The “Cliff” Effect?

Imagine enjoying your retirement in Phoenix, AZ, or Los Angeles, CA, only to receive a surprise bill. That is the reality of IRMAA.

IRMAA is a surcharge added to Medicare Part B (Medical) and Medicare Part D (Prescription Drugs). Unlike standard income tax, which is marginal (where you only pay higher rates on the income above the threshold), IRMAA acts like a cliff.

The Cliff Warning: If your MAGI is even $1.00 over the threshold, you are bumped into the next tier and must pay the higher premium for the entire year. For example, if you are single and your MAGI is $111,001, you pay the Tier 2 price, not the Tier 1 price.

How MAGI is Calculated

The cornerstone of your premium calculation is Modified Adjusted Gross Income (MAGI). It is different from the MAGI used for Affordable Care Act credits. For Medicare, the formula is:

Where:

-

AGI (Adjusted Gross Income): This is found on line 11 of your IRS Form 1040. It includes wages, dividends, capital gains, and taxable Social Security.

-

Tax-Exempt Interest: Interest from municipal bonds, which is usually tax-free for federal income tax purposes, is added back in for Medicare calculations.

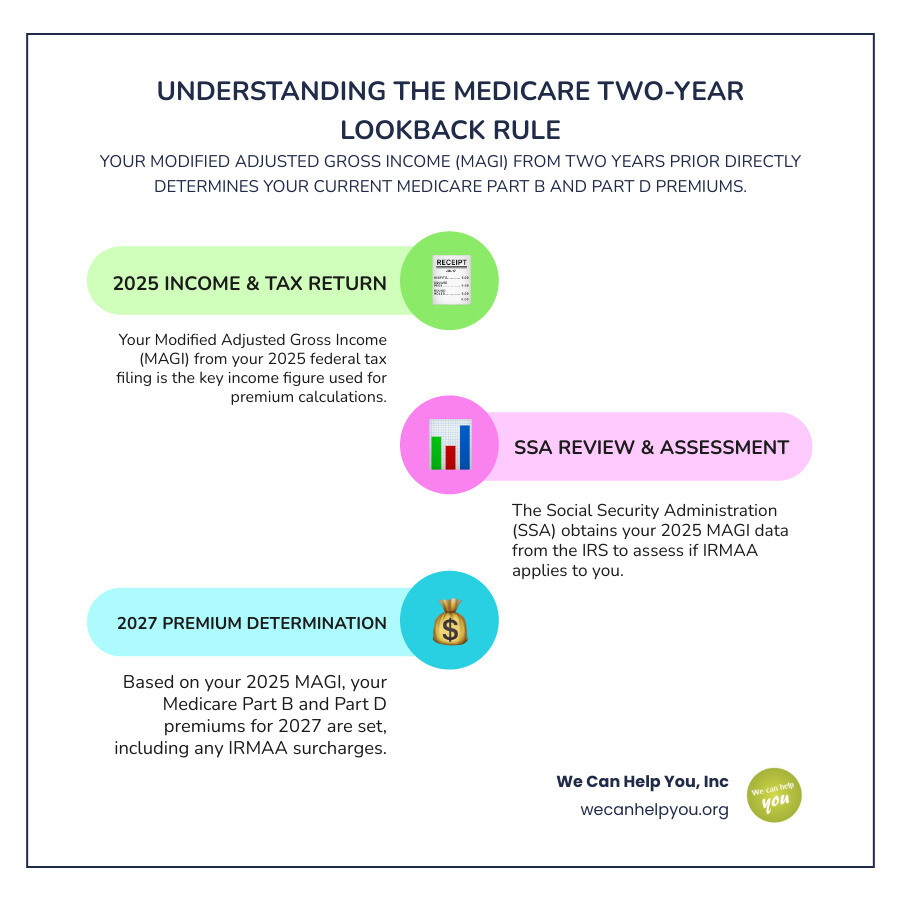

The Two-Year Lookback Rule

The Social Security Administration (SSA) determines your premiums using tax data from two years prior because that is the most recent verified data available from the IRS.

-

2025: You earn income, sell assets, or take distributions.

-

2026: You file your 2025 tax return.

-

2027: You pay Medicare premiums based on that return.

This lag is why proactive planning in 2025 is critical. You cannot change your 2025 income once the year ends.

Proactive Strategies to Lower Your 2027 Premiums

You have a window of opportunity right now to influence your future costs. Here is how to keep your MAGI in check.

1. Strategic Roth Conversions

If you are in a “gap year” (retired but not yet taking RMDs), you might consider converting Traditional IRA funds to a Roth IRA.

-

The Risk: The conversion counts as income now, raising your current MAGI.

-

The Reward: Future withdrawals from the Roth IRA are tax-free and do not count toward MAGI, potentially keeping you in a lower bracket forever once the conversion is done.

2. Qualified Charitable Distributions (QCDs)

If you are age 70½ or older, a QCD is a powerful tool. You can transfer up to $105,000 (indexed for inflation) directly from your IRA to a qualified charity.

-

The Benefit: This counts toward your Required Minimum Distribution (RMD) but is excluded from your AGI. This lowers your MAGI dollar-for-dollar compared to taking the cash and donating it later.

3. Tax-Gain Harvesting & Asset Location

-

Harvesting: If you have investments with losses, selling them can offset capital gains, lowering your AGI.

-

Asset Location: Keep high-yield assets (like bonds or REITs) in tax-deferred accounts (IRAs) so the income doesn’t hit your tax return annually. Keep growth stocks in taxable accounts where you control when to sell and realize gains.

Appealing Your IRMAA Determination

Life is unpredictable. If your income in 2025 was high, but your income in 2027 has dropped significantly due to a specific life event, you do not have to accept the high premiums. You can file an appeal using Form SSA-44.

Qualifying Life-Changing Events

You cannot appeal just because your income dropped; it must be tied to one of these events:

-

Marriage

-

Divorce or Annulment

-

Death of a Spouse

-

Work Stoppage (Retirement)

-

Work Reduction (Moving to part-time)

-

Loss of Income-Producing Property

-

Loss of Pension Income

Example: You retire in 2026. Your 2025 income (while working) was high, triggering IRMAA for 2027. Since you have experienced a “Work Stoppage,” you can file Form SSA-44 to ask Medicare to use your current lower income estimate instead of the 2025 tax return.

Frequently Asked Questions

Q: Will my Medicare Advantage (Part C) premium also increase?

A: Yes and no. The plan’s premium itself doesn’t change based on income, but you must still pay the Part B IRMAA and Part D IRMAA to the government, even if you are on a private Advantage plan.

Q: What if I amend my 2025 tax return?

A: If you file an amended return that lowers your MAGI, you must proactively notify the SSA. They do not automatically check for amended returns. Provide them with a copy of the IRS acknowledgement to get your premiums adjusted.

Q: Does a one-time capital gain count?

A: Yes. Selling a vacation home or a large amount of stock in 2025 will inflate your MAGI and could trigger IRMAA for 2027. Installment sales or timing the sale can help manage this spike.

Conclusion: Take Control of Your 2027 Costs

Navigating Medicare premiums based on income 2027 can feel like a maze, but you have the map. The decisions you make regarding your portfolio, retirement withdrawals, and charitable giving in 2025 will set the price tag for your healthcare in 2027.

At We Can Help You., our mission as a 501(c)(3) nonprofit is to provide the education you need for a secure retirement. Whether you live in Arizona, Florida, Illinois, or anywhere across the US, we are here to help you keep more of your hard-earned money.